LIFO Perpetual Inventory: Principles, Calculations, and Impacts

However, we’ve developed a spreadsheet to help you track LIFO layers if you don’t have the appropriate software. So let’s start on July 1st and see what our average cost per unit was on that day. So if we took our total cost, which would be 1,000 times the $20 per unit, 1000 \times 20 where the total cost is going to be $20,000, right?

Documenting Transactions and Purchases

- The company uses a periodic inventory system to account for sales and purchases of inventory.

- The LIFO perpetual inventory system’s influence on a company’s tax obligations is a compelling consideration for businesses.

- Changes in inventory are accurate (as long as there is no theft or damage to any goods) and can be easily accessed immediately.

- This discussion will explore various aspects of the LIFO perpetual inventory system, including its principles, calculations, and broader implications for businesses.

- FIFO differs in that it leads to a higher closing inventory and a smaller COGS.

Let’s say you’ve sold 15 items, and you have 10 new items in stock and 10 older items. You would multiply the first 10 by the cost of your newest goods, and the remaining 5 by the cost of your older items to calculate your Cost of Goods Sold using LIFO. On December 31, 2016, a physical count of inventory was made and 120 units of material were found in the store room. A trading company has provided the following data about purchases and sales of a commodity made during the year 2016. Considering that deflation is the item’s price decrease through time, you will see a smaller COGS with the LIFO method. Also, you will see a more significant remaining inventory value because the most expensive items were bought and kept at the very beginning.

Perpetual Inventory Average Cost

For the past 52 years, Harold Averkamp (CPA, MBA) hasworked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. This is slightly different from the amount calculated on the perpetual basis which worked out to be $2300. Therefore, the value of ending inventory under both systems will usually differ when applying the LIFO basis. Let’s see the LIFO method in action in a more complete example below that includes a range of transactions.

3 Calculate the Cost of Goods Sold and Ending Inventory Using the Perpetual Method

Also, we will see how to calculate its cost of goods sold using LIFO, and show how to use our LIFO calculator online to make more profits. Let’s repeat Step 2 to account for the sale that occured on January 15. We will only use the units in beginning inventory if the most recent purchases aren’t enough to cover the sale. Unlike, perpetual inventory charitable contributions system that calculates the value of inventory after each issue, the periodic system provides a one-time calculation of the inventory value at the end of the period. Deducting the cost of sales from the sales revenue gives us the amount of gross profit. For example, on January 6, a total of 14 units were sold, but none were acquired.

Calculations of Costs of Goods Sold, Ending Inventory, and Gross Margin, Specific Identification

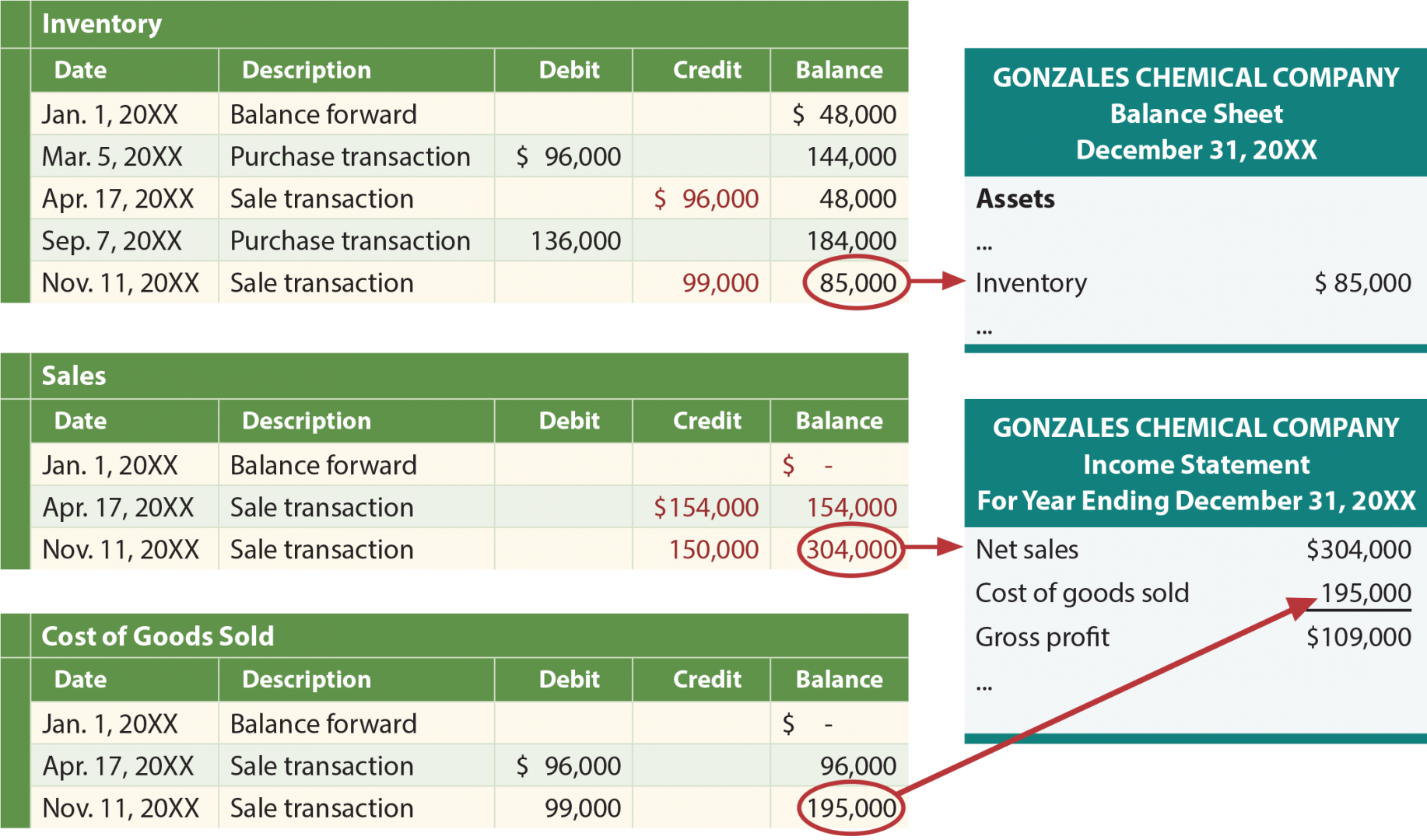

Once those units were sold, there remained 30 more units of the beginning inventory. The second sale of 180 units consisted of 20 units at $21 per unit and 160 units at $27 per unit for a total second-sale cost of $4,740. Thus, after two sales, there remained 10 units of inventory that had cost the company $21, and 65 units that had cost the company $27 each. Ending inventory was made up of 10 units at $21 each, 65 units at $27 each, and 210 units at $33 each, for a total specific identification perpetual ending inventory value of $8,895. In a perpetual inventory system, inventory records are continuously updated with each purchase and sale, providing real-time data on inventory levels and cost of goods sold (COGS).

What Is the Weighted Average Cost Perpetual Inventory Method?

Perpetual inventory has been seen as the wave of the future for many years. It has grown since the 1970s alongside the development of affordable personal computers. These UPC codes identify specific products but are not specific to the particular batch of goods that were produced. This more specific information allows better control, greater accountability, increased efficiency, and overall quality monitoring of goods in inventory. The technology advancements that are available for perpetual inventory systems make it nearly impossible for businesses to choose periodic inventory and forego the competitive advantages that the technology offers.

LIFO stands for last-in, first-out, and it’s an accounting method for measuring the COGS (costs of goods sold) based on inventory prices. The particularity of the LIFO method is that it takes into account the price of the last acquired items whenever you sell stock. During periods of inflation, a LIFO system may be more appropriate for companies that do not wish to pay as much in taxes, because it will show a higher COGS expense and a lower net income. Therefore, your company has a lower tax liability in a LIFO system, because businesses get taxed on profit. The Internal Revenue Service allows companies to use LIFO in their tax accounting, even when they use FIFO in their financial statements.

Preparing a schedule of LIFO layers before updating perpetual records for a sale is important in making sure you take COGS from the most recent layer. Take note that you have to repeat this step before you make entries to LIFO layers. This schedule will serve as your guide to what layer needs to be updated. Figure 10.20 shows the gross margin, resulting from the weighted-average perpetual cost allocations of $7,253. Let’s return to The Spy Who Loves You Corporation data to demonstrate the four cost allocation methods, assuming inventory is updated on an ongoing basis in a perpetual system. In most cases, LIFO will result in lower closing inventory and a larger COGS.

Leave a Reply